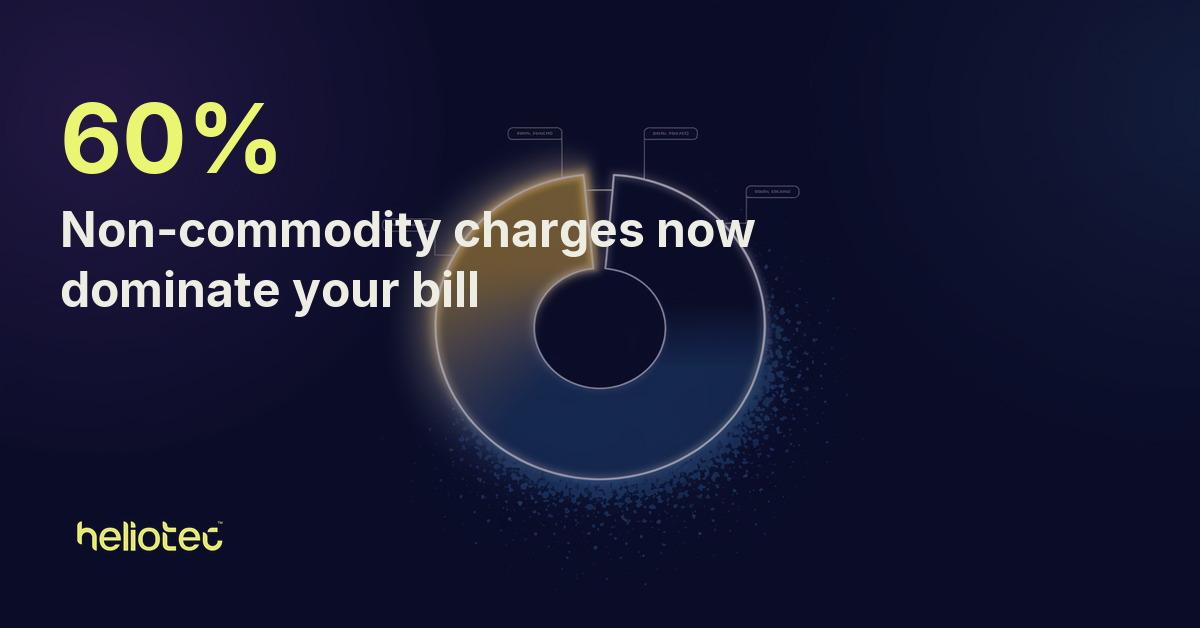

Your Energy Contract Covers Less Than Half the Bill. Here’s What Manages the Rest.

There is a persistent assumption in commercial energy management that getting procurement right is getting energy right. Lock in a competitive contract, hedge your commodity exposure, review at renewal — job done. Cornwall Insight’s 2026 market outlook challenges that assumption directly: non-commodity charges are forecast to represent nearly 60% of a typical business electricity bill next year. The contract your team spent months negotiating now governs less than half of what you actually pay.

The Bill Has Quietly Restructured Around You

Non-commodity charges are not new, but their trajectory has become impossible to ignore. Transmission network use of system (TNUoS) costs are rising sharply. The new Nuclear RAB levy introduces a further fixed obligation that flows through to business customers regardless of how well they buy in the wholesale market. Widening exemption schemes offer some relief — but Cornwall Insight notes that around 500 energy-intensive businesses qualify for meaningful protection. The vast majority of commercial and industrial customers sit outside that boundary, absorbing the full escalation with no structural buffer.

This is not a procurement problem. It is an operational and financial exposure that procurement cannot solve. The charges that now dominate the bill are driven by when and how you consume electricity — your demand profile, your flexibility, your behaviour at peak periods — not by the price per unit you negotiated twelve months ago.

Waiting for Government Intervention Is a Strategy With a Poor Track Record

Cornwall Insight anticipates further government intervention in non-commodity cost structures. That may well materialise. But intervention, when it arrives, tends to target the systemic architecture of the charging framework — not the individual consumption patterns that determine what any given business actually pays within that framework. Waiting is a passive position in an active cost environment.

The businesses that will be best placed in 2026 and beyond are those that have already built the capability to respond dynamically — shifting load away from high-cost periods, identifying waste that compounds across complex tariff structures, and treating energy as something to be managed in real time rather than reviewed quarterly. That capability does not emerge from a contract. It emerges from visibility and control over consumption behaviour.

AI Makes the Non-Commodity Portion Manageable

This is precisely the gap that Heliotec was built to close. Our AI energy management platform continuously monitors consumption across sites, identifies the patterns that drive avoidable non-commodity cost exposure, and surfaces the actions — automated or recommended — that reduce that exposure. Where a procurement strategy stops at the meter, Heliotec starts there.

For energy managers, this means moving from reactive bill analysis to proactive cost control. For C-suite leaders, it means that energy cost is no longer a line item that simply grows with the market — it becomes something the business has genuine influence over, even as the external charging landscape shifts.

The non-commodity forecast from Cornwall Insight is a structural signal, not a temporary blip. The charging regime is being redesigned around a grid that needs demand flexibility. Businesses that align their operations with that redesign will find cost advantage in it. Those that don’t will simply pay more.

Conclusion

Energy strategy in 2026 requires two things working together: a well-structured commodity procurement position, and an active management capability for everything the contract does not cover. The second part of that equation has been underinvested in for years. Cornwall Insight’s analysis makes the cost of that underinvestment legible. The question now is not whether non-commodity charges matter — it is whether your organisation has the tools to do something about them.