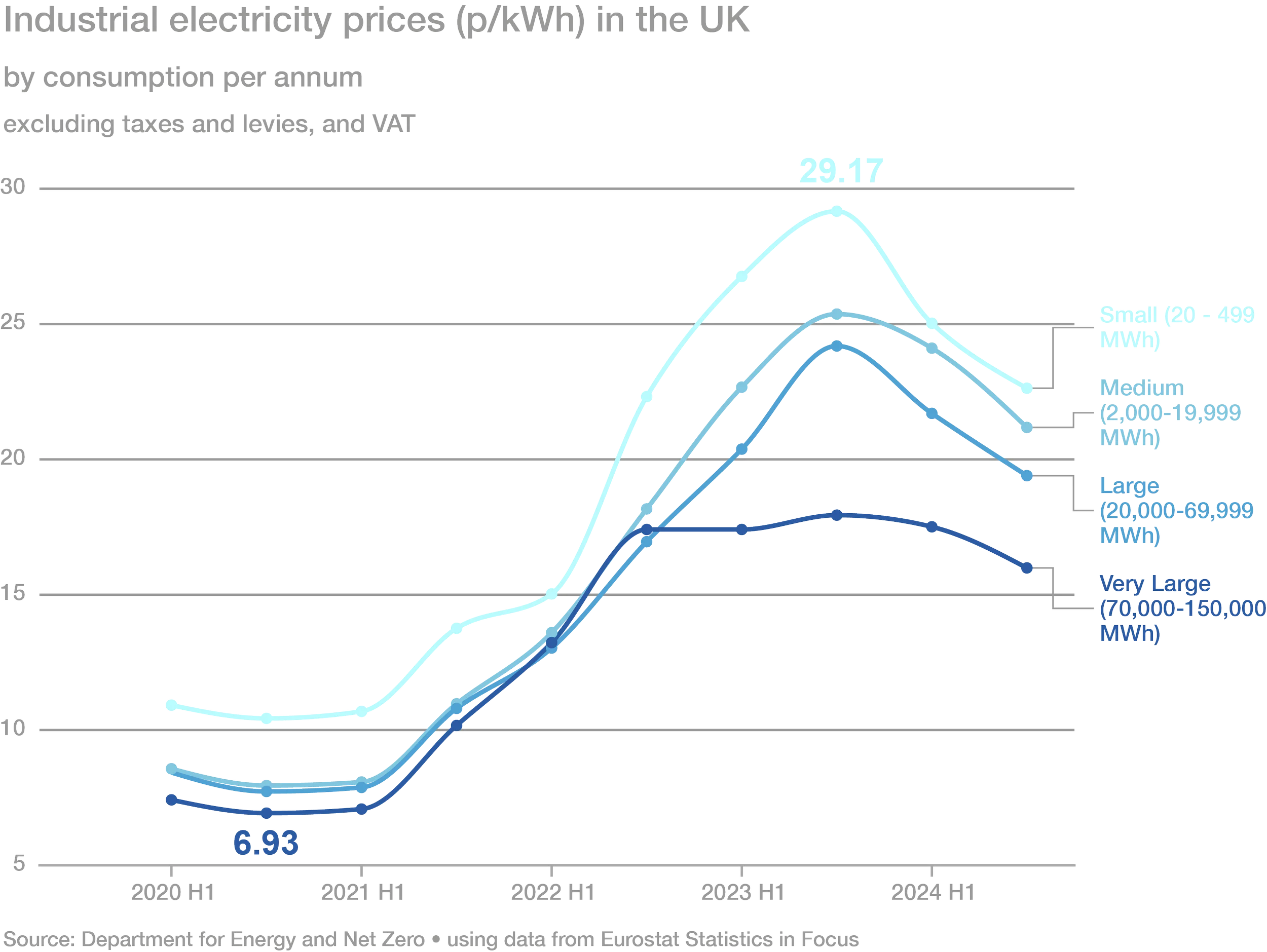

Four separate developments are reshaping what UK businesses pay for electricity, and what’s available to balance that cost. Here’s a roundup of where each stands.

TNUoS: Network Charges Rising Sharply

NESO published final Transmission Network Use of System (TNUoS) rates for the charging year starting in April 2026, confirming a rise of more than 60% year-on-year. TNUoS is the charge businesses pay for using the electricity transmission network, and it’s calculated in part around specific demand periods — meaning a site’s consumption pattern, not just its total volume, affects it. Further decisions affecting April 2027 charges are expected later this year, making this a recurring — rather than one-off — adjustment.

RIIO-3: The New Price Control Period Pushing Gas Network Costs Up

Alongside TNUoS, gas network charges for the first year of the new RIIO-3 regulatory period have followed a similar curve — in line with draft proposals, but still a significant increase on current rates. RIIO-3 sets how much network operators can charge to fund infrastructure investment over the coming price control period, and its early costs landed on business bills from April this year alongside the TNUoS rise, combining the burden from both charges.

The Demand Flexibility Service: A Growing Revenue Option

The Demand Flexibility Service (DFS) — NESO’s procedure for rewarding businesses that shift electricity use to help balance the grid — expanded from 9th April. The service now rewards businesses for using more electricity at times of excess supply, not just less at peak times. It has also moved to zonal procurement and lowered its eligibility threshold from 1MW to 0.1MW, to a wider range of commercial sites.

Over 2.46 million businesses and consumers have signed up to date. For businesses with flexibility in when they consume electricity, DFS is increasingly a means of revenue — but participating requires half-hourly metering and the ability to shift consumption when asked, which in practice means knowing a site’s consumption patterns well enough to commit.

The Net Effect On Price Trends

Put together, these developments point in a specific direction: the largest cost movements are coming from network and policy charges, not from wholesale energy prices. Non-commodity costs are on track to make up close to 60% of a typical business electricity bill. Cost control has to move away from negotiating a better unit rate, and towards understanding and managing when and how a site consumes energy.

What This Means

Businesses reviewing their energy strategy this year are dealing with two forces at once: rising fixed and network costs that a good tariff won’t counterbalance, and a growing set of flexibility mechanisms that reward businesses able to demonstrate and act on their consumption patterns. Knowing exactly how and when a site uses energy is now relevant to managing cost and as a means of new revenue, not one or the other.

Sources: NESO TNUoS charging announcements and RIIO-3 publications; NESO Demand Flexibility Service design updates (April 2026); Ofgem approval of evolved DFS design (March 2026); Cornwall Insight 2026 market forecasts.